Simulator Market Outlook: Size, Share, Trends & Growth Analysis (2024-2029)

The market report presents a thorough analysis segmented by Platform (Air, Land, Maritime); by Type (Flight Training Devices, Full Flight Simulators, Full Mission Flight Simulators, Fixed Base Simulators, Air Traffic Control Simulators, Others); by Application (Military Training, Commercial Training); by Technique (Live, Virtual and Constructive, Synthetic Environment Simulator, Gaming Simulator); by Geography (North America, South America, Asia Pacific, Europe, The Middle East, Africa).

Outlook

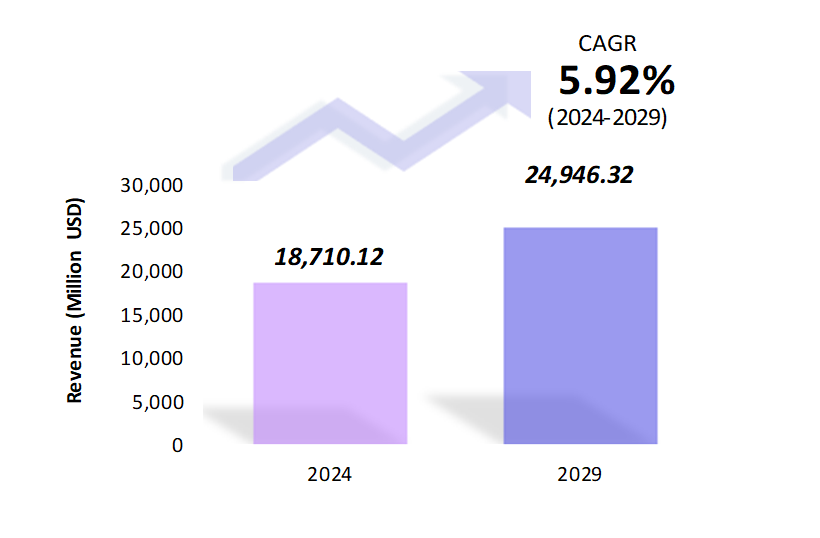

- The simulator market is estimated to be at USD 18,710.12 Mn in 2024 and is anticipated to reach USD 24,946.32 Mn in 2029.

- The simulator market is registering a CAGR of 5.92% during the forecast period 2024-2029.

- The simulator market is driven by increasing demand across industries such as aviation, military, healthcare, and gaming due to the need for cost-effective and safe training solutions. Advancements in Artificial Intelligence AI, cloud-based platforms, and extended reality are enhancing simulation capabilities, offering more immersive and adaptive experiences.

Request a free sample.

Ecosystem

- The participants in the global simulator industry are always developing their strategies to preserve a competitive advantage.

- These companies focus on innovation, integrating AI and Virtual Reality VR technologies to offer advanced simulation solutions. Smaller firms and startups are also emerging, leveraging niche applications in gaming and healthcare.

- Several important entities in the simulator market include CAE Inc.; Thales Group; L3Harris Technologies, Inc.; Saab AB; Indra Sistemas, S.A.; and others.

Ask for customization.

Findings

| Attributes | Values |

|---|---|

| Historical Period | 2018-2022 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Market Size (2024) | USD 18,710.12 Mn |

| Market Size (2029) | USD 24,946.32 Mn |

| Growth Rate | 5.92% CAGR from 2024 to 2029 |

| Key Segments | Platform (Air, Land, Maritime); Type (Flight Training Devices, Full Flight Simulators, Full Mission Flight Simulators, Fixed Base Simulators, Air Traffic Control Simulators ,Others); Application (Military Training, Commercial Training); Technique (Live, Virtual and Constructive, Synthetic Environment Simulator, Gaming Simulator); Geography (North America, South America, Asia Pacific, Europe, The Middle East, Africa) |

| Key Vendors | CAE Inc.; Thales Group; L3Harris Technologies, Inc.; Saab AB; Indra Sistemas, S.A. |

| Key Countries | The US; Canada; Mexico; Brazil; Argentina; Colombia; Chile; China; India; Japan; South Korea; The UK; Germany; Italy; France; Spain; Turkey; UAE; Saudi Arabia; Egypt; South Africa |

| Largest Market | North America |

Get a free quote.

Trends

- Cloud-Based Simulators: Cloud technology enables remote access and real-time updates in simulation training, significantly enhancing accessibility and collaboration for global teams. This innovation allows trainees to access training modules from any location, streamlining coordination across different time zones and regions. For instance, Boeing has integrated cloud-based simulators for pilot training, which allows trainees to practice from anywhere.

- AI-Powered Adaptive Learning: Artificial intelligence is now used to create adaptive learning environments within simulators, where training scenarios adjust based on the trainee’s performance. CAE Inc. is employing AI to offer personalized training modules for military and commercial pilots.

- XR (Extended Reality) Integration: Simulators are incorporating extended reality (a combination of AR and VR) for a more immersive training experience. XR-based simulators, like those used in healthcare for surgical training, provide hands-on practice in a virtual space, which improves skill transfer without physical risks.

Speak to analyst.

Catalysts

- Rising Demand for Pilot Training: The rapid expansion of the global aviation industry, particularly in emerging markets, is creating an unprecedented need for trained pilots. Airbus forecasts the requirement of over 600,000 new pilots by 2040, fueling the adoption of advanced flight simulators that offer immersive and scalable training solutions. These simulators allow airlines to train pilots efficiently without the risks and costs of in-flight sessions.

- Need for Low-Cost Military Training: Military organizations are increasingly relying on simulators to significantly reduce the expenses linked to live combat exercises. Simulators provide a cost-effective alternative for comprehensive training. For instance, NATO’s use of advanced combat simulation systems enables realistic, scenario-based training, which helps soldiers refine tactical skills without deploying actual combat resources or risking safety.

- Safety of Simulator-Based Training: Simulation technology offers a safe, controlled environment for practicing high-risk procedures or operations. In the healthcare sector, surgical simulators have become integral to training, which enables medical professionals to master complex techniques without endangering patients. Simulators replicate real-world conditions that reduce error rates and enhance confidence before living interventions.

Inquire before buying.

Restraints

- Stringent Regulatory Approvals: Simulators used in industries like aviation, healthcare, and defense must meet strict regulatory standards before being implemented. Flight simulators must pass rigorous certification processes from authorities such as the Federal Aviation Administration FAA and the European Union Aviation Safety Agency EASA, which can delay product deployment and increase development costs.

- Complexity of Reducing Size and Weight of Military Simulators: Designing military simulators that are both portable and high-performance presents significant engineering challenges. Reducing size and weight while maintaining realism and functionality is crucial for on-site training in remote locations, but achieving this balance often leads to higher development complexities and costs.

- High Cost of Gaming Simulators: Advanced gaming simulators, especially those used for esports and professional training, come with a high price tag due to the sophisticated hardware and software required. The investment in high-end VR headsets, haptic feedback systems, and motion platforms makes these simulators prohibitively expensive for casual users or smaller gaming centers.

Personalize this research.

Hotspot

Explore purchase options.

Table of Contents

| 1. Introduction 1.1. Research Methodology 1.2. Scope of the Study 2. Market Overview / Executive Summary 2.1. Global Simulator Market (2018 – 2022) 2.2. Global Simulator Market (2023 – 2029) 3. Market Segmentation 3.1. Global Simulator Market by Platform 3.1.1. Air 3.1.2. Land 3.1.3. Maritime 3.2. Global Simulator Market by Type 3.2.1. Flight Training Devices 3.2.2. Full Flight Simulators 3.2.3. Full Mission Flight Simulators 3.2.4. Fixed Base Simulators 3.2.5. Air Traffic Control Simulators 3.2.6. Others 3.3. Global Simulator Market by Application 3.3.1. Military Training 3.3.2. Commercial Training 3.4. Global Simulator Market by Technique 3.4.1. Live, Virtual and Constructive 3.4.2. Synthetic Environment Simulator 3.4.3. Gaming Simulator 4. Regional Segmentation 4.1. North America 4.1.1. The US 4.1.2. Canada 4.1.3. Mexico 4.2. South America 4.2.1. Brazil 4.2.2. Argentina 4.2.3. Colombia 4.2.4. Chile 4.2.5. Rest of South America 4.3. Asia Pacific 4.3.1. China 4.3.2. India 4.3.3. Japan 4.3.4. South Korea 4.3.5. Rest of Asia Pacific 4.4. Europe 4.4.1. The UK 4.4.2. Germany 4.4.3. Italy 4.4.4. France 4.4.5. Spain 4.4.6. Rest of Europe 4.5. The Middle East 4.5.1. Turkey 4.5.2. UAE 4.5.3. Saudi Arabia 4.5.4. Rest of the Middle East 4.6. Africa 4.6.1. Egypt 4.6.2. South Africa 4.6.3. Rest of Africa 5. Value Chain Analysis of the Global Simulator Market 6. Porter Five Forces Analysis 6.1. Threats of New Entrants 6.2. Threats of Substitutes 6.3. Bargaining Power of Buyers 6.4. Bargaining Power of Suppliers 6.5. Competition in the Industry 7. Trends, Drivers and Challenges Analysis 7.1. Market Trends 7.1.1. Market Trend 1 7.1.2. Market Trend 2 7.1.3. Market Trend 3 7.2. Market Drivers 7.2.1. Market Driver 1 7.2.2. Market Driver 2 7.2.3. Market Driver 3 7.3. Market Challenges 7.3.1. Market Challenge 1 7.3.2. Market Challenge 2 7.3.3. Market Challenge 3 8. Opportunities Analysis 8.1. Market Opportunity 1 8.2. Market Opportunity 2 8.3. Market Opportunity 3 9. Competitive Landscape 9.1. CAE Inc. 9.2. Thales Group 9.3. L3Harris Technologies, Inc. 9.4. Saab AB 9.5. Indra Sistemas, S.A. 9.6. Company 6 9.7. Company 7 9.8. Company 8 9.9. Company 9 9.10. Company 10 |

Know the research methodology.

Simulator Market – FAQs

1. What is the current size of the simulator market?

Ans. In 2024, the simulator market size is USD 18,710.12 Mn.

2. Who are the major vendors in the simulator market?

Ans. The major vendors in the simulator market are CAE Inc.; Thales Group; L3Harris Technologies, Inc.; Saab AB; Indra Sistemas, S.A.

3. Which segments are covered under the simulator market segments analysis?

Ans. The simulator market report offers in-depth insights into Platform, Type, Application, Technique, and Geography.